February 2026 Newsletter

Welcome to the February edition of the Engage Strategic newsletter. Today, we focus on the recent US-Australia Critical minerals program.

Who are we?

We are experienced ASX market professionals (former Executives, Directors and Brokers). Our Service Partners are:

Joe Kaderavek (joe.kaderavek@engageir.com) 0434 563 456

John Wardman (john.wardman@engageir.com) 0403 381 993

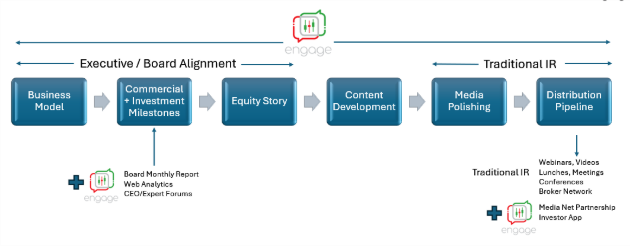

Engage Strategic is our core service, working with Executives and Boards to develop ASX company business models, key milestones, equity story and generating ASX/media content. Traditional IR services just 'polish' and distribute.

The Engage Investor App is a new product we are developing that will revolutionise the way companies and shareholders engage with one another - stay tuned for more news about this.

Recent US-Australia Critical Minerals Program

Author: Joe Kaderavek

Key Outcomes:

The world needs alternatives to China.

The US is now deploying capital dedicated to building them.

Australian juniors are positioned to be at the centre of that transformation.

The global rare earths landscape has shifted rapidly, and nowhere is that more evident than in the deepening US-Australian partnership on critical minerals. What began as diplomatic alignment has matured into a fully capitalised industrial strategy, amplified under Trump era agreements that now function as a de facto funding for non Chinese supply.

The centrepiece is the US$8.5 billion US-Australia critical minerals pact announced at the Trump-Albanese White House summit - a program designed to build, safeguard, and subsidise Western rare earth supply chains. The agreement commits both nations to invest at least US$1B each within six months, unlocking a pipeline of Australian mining and processing projects and creating a structured route for juniors to secure US offtake, funding, and long term contracts.

For investors, this is transformative. The pact introduces:

Price floors to protect producers from market manipulation and undercutting;

Geological mapping cooperation to accelerate project definition;

Restrictions on adversarial asset acquisition, directly shielding Australian juniors from predatory capital;

Integrated downstream planning, including magnet supply chain build outs in the US and Australia.

This is occurring against the backdrop of China’s tightening export controls, which target seven key heavy rare earths and continue to disrupt global supply chains. Despite a temporary pause on some new restrictions, analysts emphasise China’s actions are tactical, not structural: its dominance - 85-90% of global processing - remains the world’s critical vulnerability.

For Australian juniors, this combination of geopolitical pressure + US capital + Chinese export risk is creating the most favourable strategic environment in decades. The US defence sector, EV manufacturers, and magnet producers are actively searching for long term, non Chinese partners - and Australia is the preferred jurisdiction due to its deposits, regulatory stability, and alignment with Western security interests.

Major institutions now forecast that Australia could grow its global share of rare earth supply to 20–25% by 2035, nearly double current levels. At the same time, Macquarie forecasts ongoing NdPr deficits through 2027, reinforcing long term price strength and improving project bankability.

As an investor relations firm, we view these new US-Australian CM programs not simply as policy announcements but as market moving funding signals. They de risk Australian rare earths development, attract institutional capital, and provide a narrative of strategic necessity rather than speculative opportunity.

Please forward this link on to others if they would like to receive future versions of this newsletter: Engage Strategic Newsletter Sign-Up.